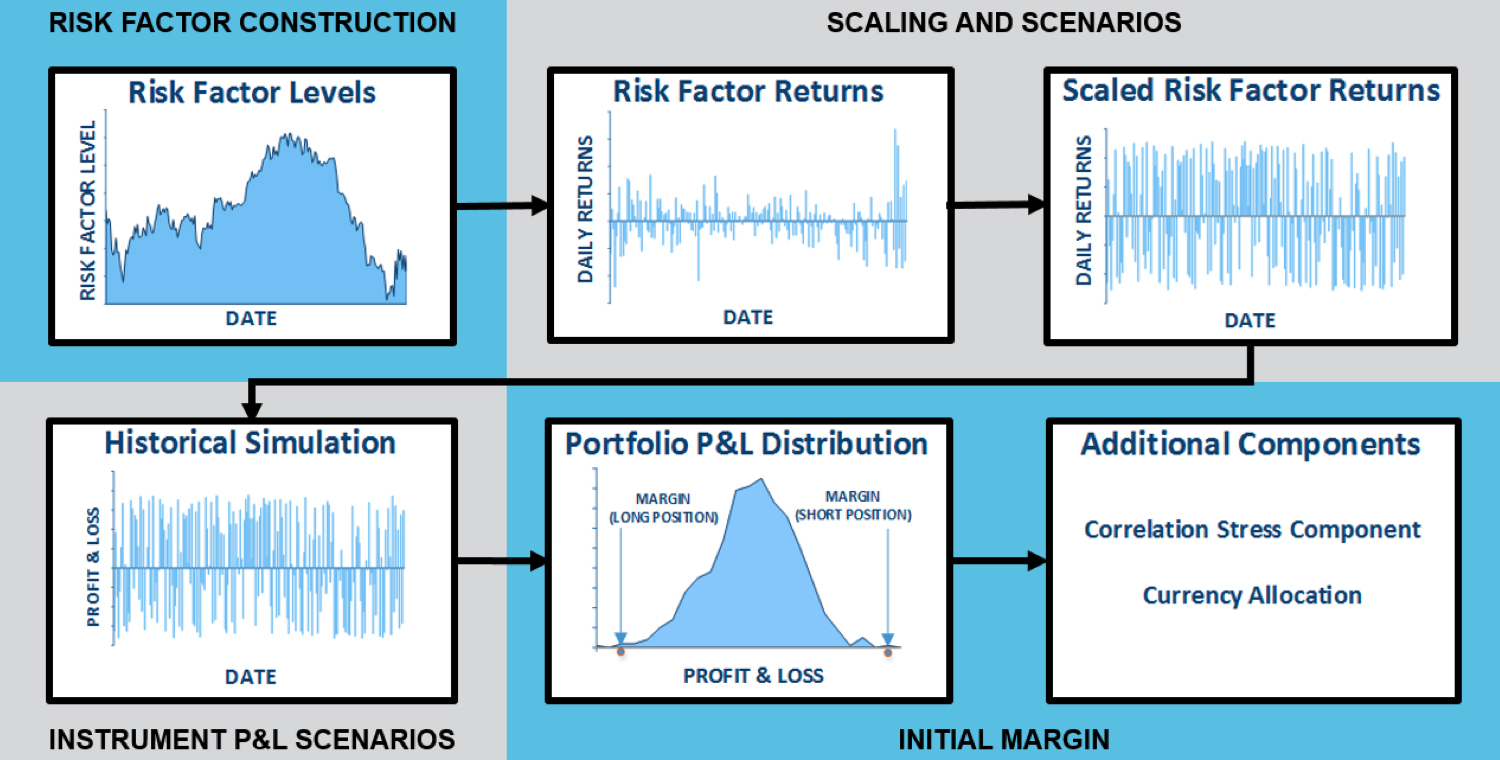

IRM 2.0 Initial Margin Flow

Risk Factors are representations of the factors driving valuation changes. They may be a price, return or rate.

Risk Factors are constructed from prices of observable instruments.

The return Risk Factors are scaled in order to produce scenarios that reflect current market volatility and incorporate various risk and regulatory requirements.

Instrument P&Ls simulations are generated by using top day risk factors derived prices, and scenario prices derived using scaled risk factor scenarios. Pricing functions are used in the transformation of the Top Day Risk Factors (Base Price) as well as Scaled Scenarios (Simulated Price) back to observable instrument prices.

The instrument P&L simulations are aggregated at the portfolio level and then combined with other components designed to comply with regulatory and risk requirements producing a final initial margin.

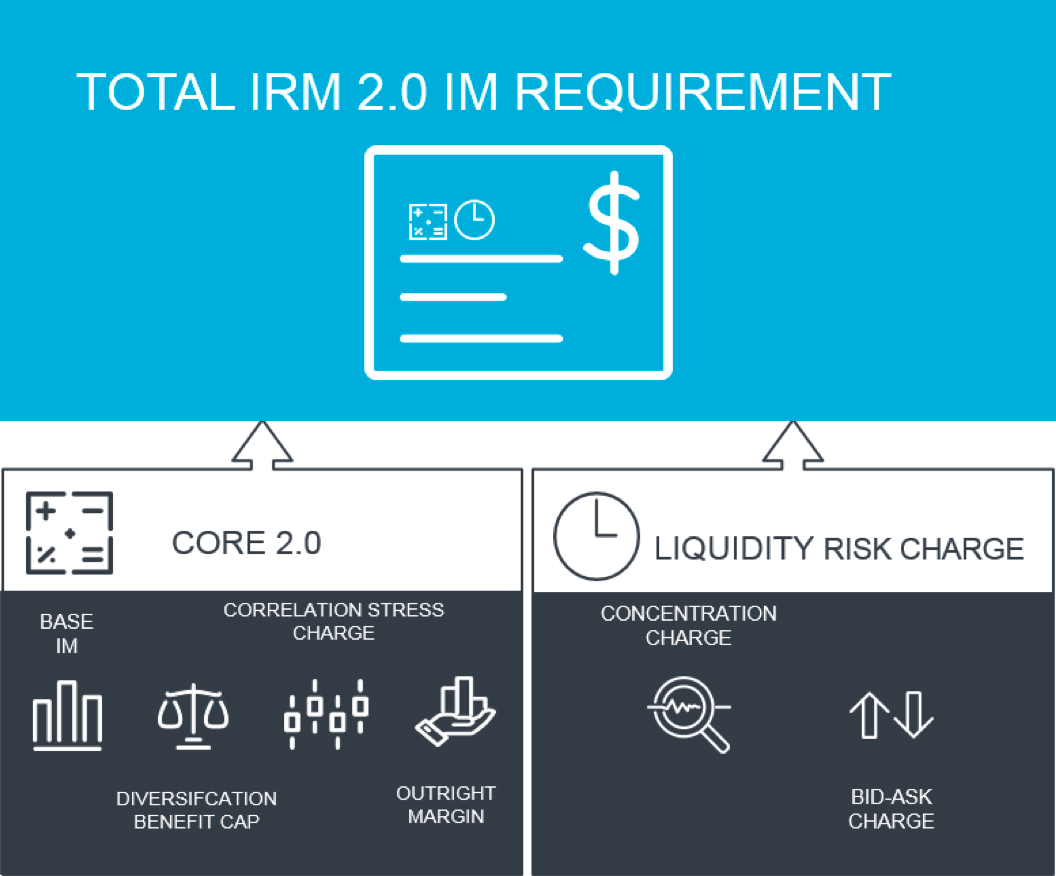

IRM 2.0 Model Components

The overall IRM 2.0 portfolio margin requirement comprises two components, the portfolio’s Initial Margin (IM) and separately, the portfolio’s Liquidity Risk Charge (LRC).

In turn, the IM and LRC components encompass sub components which are designed to capture specific risk elements. Collectively, the risk elements support the deep granularity of the overall IRM 2.0 model.

IRM 2.0 IM consists of several sub components which collectively estimate portfolio market risk based upon the network of instrument pricing relationships within the portfolio.

The Base IM represents the base market risk derived from the FHS and portfolio time series returns.

The CSC incorporates the potential impact of extreme zero correlation between the portfolio instruments.

Similar to a spread charge found in IRM 1.0, the DBC value represents an increase in initial margin that ensures offsets between different product groups do not exceed specific thresholds required by regulators in certain jurisdictions.

Instruments subject to Outright Margin are margined in their own right separate from other instruments

The Liquidity Risk Charge (LRC) estimates the cost of liquidating positions over the course of the margin horizon and consists of two the sub components Concentration Charge (CC) and Bid-Ask Charge (BAC).

The CC covers the additional risk associated with liquidating concentrated positions that exceed a predetermined volume threshold.

The BAC provides protection against liquidation costs arising from crossing the bid-ask spread of any given market. The Bid-Ask Charge is applicable to all positions in all portfolios regardless of size.

Resources

IRM 2.0 Contacts

ICE Clear U.S. Operations Helpdesk:

+1 312-836-6777 / iceclearus@ice.com

ICE Portfolio Analytics for Clearing:

+1 770-738-2101(option #6) / iceclearus@ice.com